Creating Loan Estimate (LE) Templates involves tailoring templates based on specific criteria like lender, program, state, and more. These templates are crucial for accurately estimating closing costs when working on various loan scenarios.

*Only Corporate Admin may add or edit LE Templates.

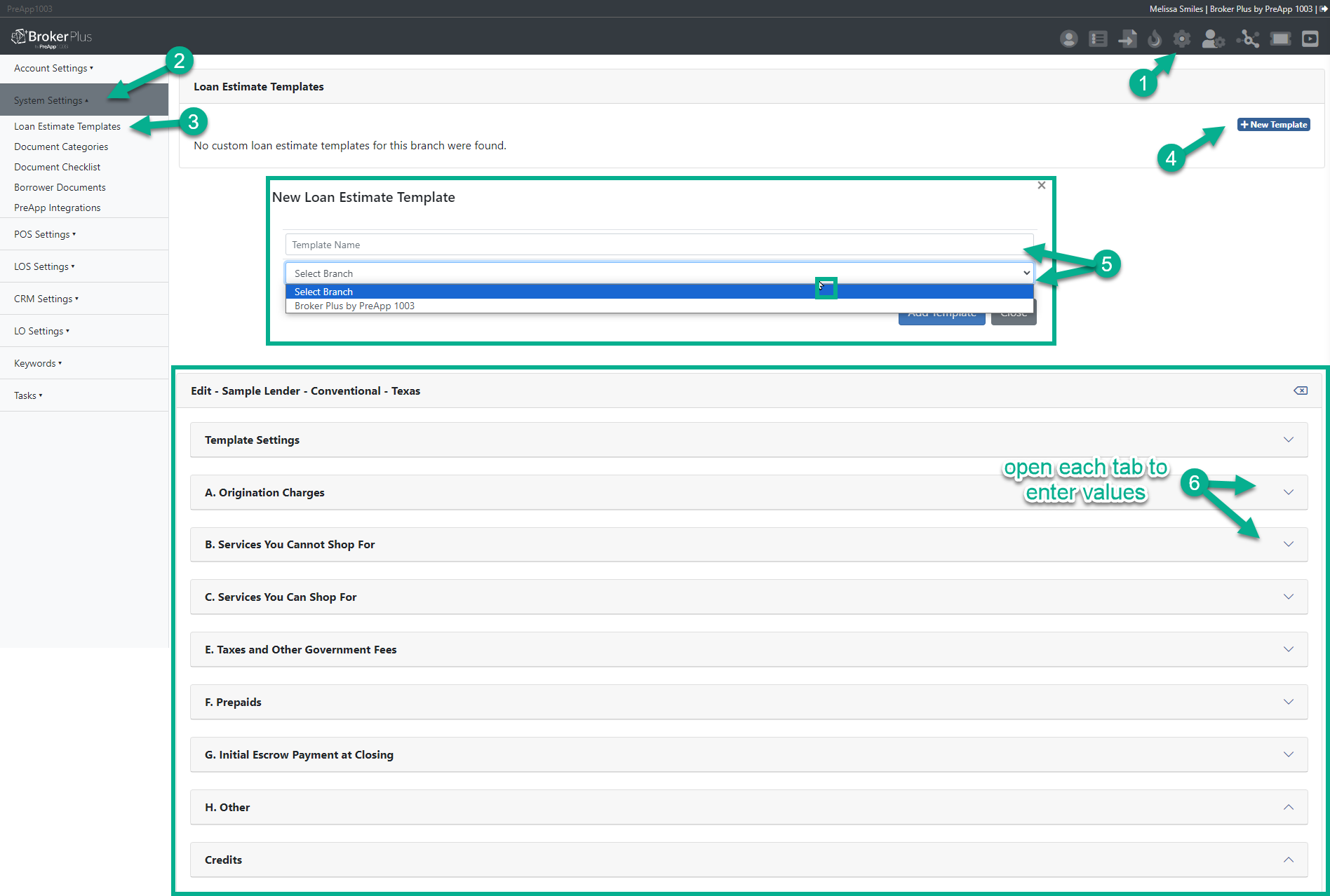

- Name your LE Templates: A common naming practice is to put the Lender’s name first, the loan type second and the state third. Example: Rocket – FHA – CA.

- Configuring your LE Templates: The recommended approach for Brokers or loan originators is to request Lender Fee Sheets directly from their lender account executives (AEs). Alternatively, if not available, past closing cost worksheets may be used as a reference. It’s important to note that while Loan Estimate (LE) Templates serve as a baseline, they may be subject to changes during the loan origination process to accommodate specific scenarios and requirements.

LE Template

LE Template

LE Template

LE TemplateLoan Costs

A. Origination Charges: Origination charges constitute the initial fees imposed by your lender, playing a significant role in your overall loan expenses. These charges may vary in their level of itemization, depending on the lender. Common origination charges encompass application fees, origination fees, underwriting fees, processing fees, verification fees, and rate-lock fees.

B. Services You Cannot Shop For: These fees are for third-party services that are required and selected by your lender. *These fees typically cannot be changed after the offer has been accepted.

C. Services You Can Shop For: These fees are also required by the lender; however, there may be flexibility in shopping for and selecting these services independently. Always verify with your lender beforehand.

Other Costs

E. Taxes and Other Government Fees: Property taxes are determined by local or state governments. To prevent unexpected surprises, reach out to your local tax authority to verify the accuracy of the estimated costs. *On the LE Template, fees are defaulted in dollar amounts, but most may be changed to percentages.

F. Prepaids: Homeowner insurance may be compared and shopped for. Anticipate paying the first 6 to 12 months of premiums by closing.

G. Initial Escrow Payment at Closing: The initial escrow deposit is the amount paid at closing to initiate your escrow account, as stipulated by your lender. This upfront sum may differ from the monthly payments designated to uphold the ongoing escrow account.

*LE Templates auto save in real time and do not have a “save” or “update” button at the bottom of the page.

Establishing Loan Estimate (LE) Templates is a critical step in delivering precise fee sheets to clients throughout the loan processing journey. Carefully entering closing costs for diverse loan scenarios, lenders, programs, states, and other relevant factors is paramount for ensuring accuracy. Thoughtful setup not only assures that clients receive comprehensive fee breakdowns tailored to their individual loan files but also streamlines the origination process for Loan Originators (LOs).

Loan Estimate Explainer by by Consumer Financial Protection Bureau.